The alarm went off at 4:47 AM in trading rooms from London to Singapore. Before most people had made their first coffee, the world had already changed.

Overnight, U.S. and Israeli warplanes had struck deep into Iran. Nuclear sites. Military installations. Command centres. The kind of strikes that don’t stay quiet. By the time Asian markets opened, Iran’s Islamic Revolutionary Guard Corps had made their answer clear: the Strait of Hormuz was closed. No commercial vessel would pass.

In the hours that followed, Brent crude climbed more than 10 percent. Not because of a forecast or a policy statement, but because traders were staring at something they had spent two years telling themselves would never actually happen.

The world moves roughly 20 million barrels of oil through that narrow stretch of water every single day. One fifth of everything the global economy runs on. And on the morning of March 1, 2026, Iran had just turned it into a war zone.

The barrel had been sitting on a knife’s edge for months. Now someone had kicked the table.

The Chokepoint That Moves Markets

Pull up a map. Find the Persian Gulf. Now find the narrow gap at the bottom where it opens to the sea. That gap is 21 miles wide at its tightest point. That is the Strait of Hormuz, and it is the single most consequential chokepoint in the global economy.

Every major oil producer in the Gulf sends their exports through it. Saudi Arabia. Iraq. The UAE. Kuwait. Qatar. Iran itself. There is no other way out by sea. No alternative route. No plan B. Just this one narrow corridor, bordered on the north by the country that just declared it closed.

The pipelines that exist as workarounds tell the same story. Saudi Arabia has its East-West Pipeline running to the Red Sea, with capacity for roughly 5 million barrels a day. The UAE has a pipeline to Fujairah on the Gulf of Oman, good for about 1.5 million barrels. Together, according to the Congressional Research Service, they can move around 2.6 million barrels a day if pushed to their limits.

The Strait normally carries 20 million.

Do the math and you understand why the trading floors went quiet on March 1st.

March 2026: The Current Escalation

June 2025 was a scare. This is something else.

When the 12-Day War ended with a ceasefire, oil prices fell back almost as fast as they had risen. The market had made its call: loud conflict, no physical damage, move on. Traders had seen this script before and knew how it ended.

But this time the script is different. Hapag-Lloyd, one of the largest shipping companies on the planet, has suspended all transits through the Strait. Not rerouted. Suspended. Tankers have already been struck in the Gulf. Iran’s IRGC has not just threatened the waterway, they have declared it closed.

Goldman Sachs has run the numbers on a sustained closure. Their answer is $110 a barrel for WTI. HSBC sees $80 as the floor if the Strait is merely disrupted, not sealed.

The market is not pricing in a skirmish that will blow over by Friday. It is pricing in something longer, something with real teeth. And for the first time since this conflict began escalating in October 2023, the physical disruption that traders always assumed would never quite arrive has actually arrived.

What Drives the Spike And What Limits It

The Inflation Variable

Here is the part that might surprise you. The Dallas Fed ran the numbers on three scenarios ranging from ceasefire to full Strait closure, and even in the worst case, with oil hitting $100 a barrel, the lasting damage to U.S. headline inflation is smaller than you would expect. The reason is that America barely depends on Gulf oil anymore. The shale boom has cut U.S. imports through the Strait to around 0.5 million barrels a day, close to a 40-year low. The pain is real, but it is not 1973.

The OPEC+ Buffer

On the same weekend the strikes began, eight OPEC+ nations announced they were increasing production by 206,000 barrels a day. The timing made it feel like a response, though the meeting had been planned long before the bombs fell. The cartel holds roughly 5.4 million barrels a day of spare capacity according to the IEA, which sounds like a meaningful cushion until you read the footnote: more than 90 percent of that spare capacity sits in Gulf countries that export through the Strait. The buffer exists on paper. Behind a Hormuz blockade, it is unreachable.

Strategic Petroleum Reserves

Governments are not without options. IEA member countries were sitting on more than 1.2 billion barrels in strategic reserves at the end of Q1 2025, with roughly 400 million of those in the U.S. Strategic Petroleum Reserve. A coordinated release can calm markets and buy time, and it has worked before. But reserves are a bridge, not a solution, and the political will to drain them tends to fade faster than the crises that justify it.

China’s Exposure

China does not get to watch this one from the sidelines. The world’s largest crude importer buys more than 80 percent of Iran’s oil and routes roughly 40 percent of all its imports through the Strait of Hormuz. A prolonged closure hits Beijing with a double shock: its primary sanctioned supplier is cut off, and the main highway for its other Gulf purchases is blocked. When China scrambles for replacement barrels, every other buyer feels it too.

The Bigger Pattern: What War Actually Does to Oil

For two and a half years, the oil market watched one of the most violent regional conflicts in modern history and barely flinched. The Gaza war killed tens of thousands of people. Iran and Israel exchanged direct missile strikes for the first time ever. Houthi rebels turned the Red Sea into a shooting gallery. Egypt lost six billion dollars a year in Suez Canal revenue. And through all of it, Brent crude spent most of its time between $70 and $90 a barrel, drifting up on the bad weeks and drifting back down when nothing blew up that mattered to a pipeline. The market was not being callous. It was being precise. It watched tanker tracking data, not casualty counts. It watched export terminals, not troop movements. And as long as the oil kept flowing, it kept its nerve.

What is different today is the thing the market always said would finally break it. Not a political statement. Not a missile that lands in a desert. Vessels are being struck in the Gulf. The world’s largest shipping companies are suspending transits. The waterway that carries one fifth of global oil supply has been declared closed by the force that controls its northern shore. For two and a half years the market discounted the war because the war never touched the infrastructure. It has touched the infrastructure now.

The Bottom Line

There is a version of this that ends quickly — an off-ramp, a reopened Strait, oil back below $75 and another scare filed away as manageable. The market has banked on that version working out before, and it was right every time. But for two and a half years the war never touched the infrastructure, and now it has. Tankers are struck. The Strait is declared closed. The world’s largest shipping companies are not transiting. Goldman Sachs has written the bad version down and the number at the end of it is $110 a barrel. The oil market spent years learning to ignore this war. It is now learning what happens when the war stops ignoring it back.

Primary Sources

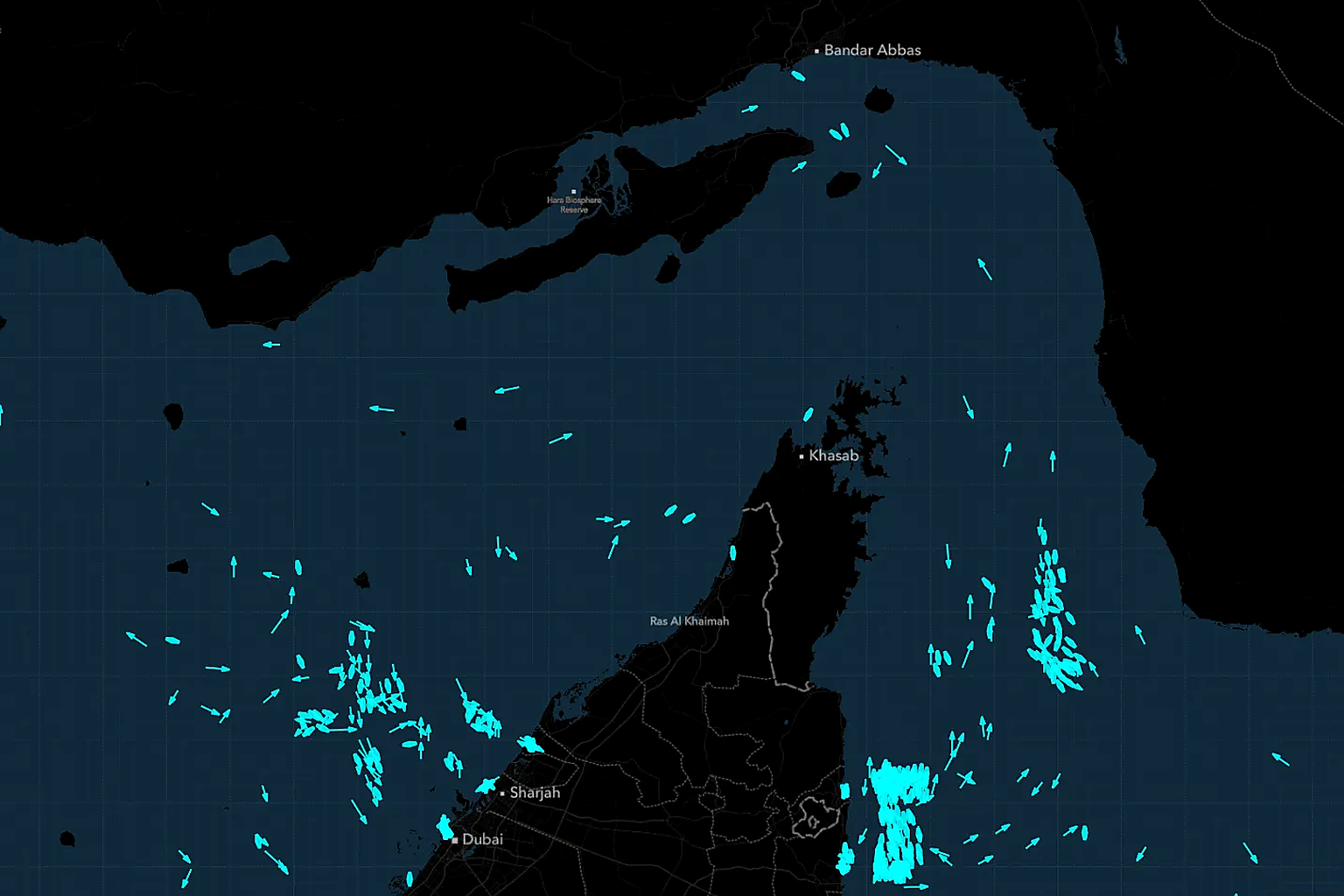

- Image: Bloomberg Finance L.P. / Mapbox / OpenStreetMap — “Waiting for Hormuz: More Oil Tankers Gather in the Persian Gulf” https://www.bloomberg.com/news/articles/2026-03-02/waiting-for-hormuz-more-oil-tankers-gather-in-the-persian-gulf

- Price & Market Data U.S. Energy Information Administration (EIA) — Strait of Hormuz Chokepoint Analysis https://www.eia.gov/todayinenergy/detail.php?id=65504

- Vortexa / EIA — Tanker Tracking & Flow Data (via EIA above)

- Investing.com — Brent Crude Futures Live Prices https://www.investing.com/commodities/brent-oil

- Scenario Analysis & Research Dallas Federal Reserve — Geopolitical Risk & Inflation Scenario Analysis https://www.dallasfed.org/research/economics/2025/0821

- Congressional Research Service — Iran Conflict and the Strait of Hormuz https://www.congress.gov/crs-product/R45281

- Georgetown Journal of International Affairs — Oil Price Risk in the Middle East https://gjia.georgetown.edu/2024/12/10/how-the-new-geopolitics-of-energy-informs-the-current-oil-price-risk-relationship-in-the-middle-east

- CSIS — Oil Market Risks Start to Resonate https://www.csis.org/analysis/oil-market-risks-start-resonate

- Breaking News & Analyst Commentary CNBC — Strait of Hormuz Closure Scenarios https://www.cnbc.com/2026/03/01/experts-weigh-potential-scenarios-for-oil-if-strait-of-hormuz-closes.html

- CNBC — Countries Most Impacted by Strait Closure https://www.cnbc.com/2026/03/03/strait-of-hormuz-closure-which-countries-will-be-hit-the-most.html

- NPR — Oil Prices Rise After Middle East Attacks https://www.npr.org/2026/03/01/nx-s1-5731584/oil-prices-iran-us-israel-attacks-war

- Yahoo Finance — Oil Prices Surge Above $80 https://finance.yahoo.com/news/oil-prices-surge-to-cross-80-after-us-iran-conflict-engulfs-middle-east-and-strait-of-hormuz-233642824.html

- Al Jazeera — Ceasefire Calms Oil Markets (June 2025) https://www.aljazeera.com/economy/2025/6/24/fragile-iran-israel-ceasefire-calms-oil-markets

- InvestmentNews — What Advisors Should Watch https://www.investmentnews.com/equities/oil-prices-leap-amid-middle-east-war-this-is-what-advisors-should-look-out-for/265489

- Institute for Energy Research — Conflict in Iran and the Oil Market https://www.instituteforenergyresearch.org/international-issues/conflict-in-iran-and-the-global-oil-market