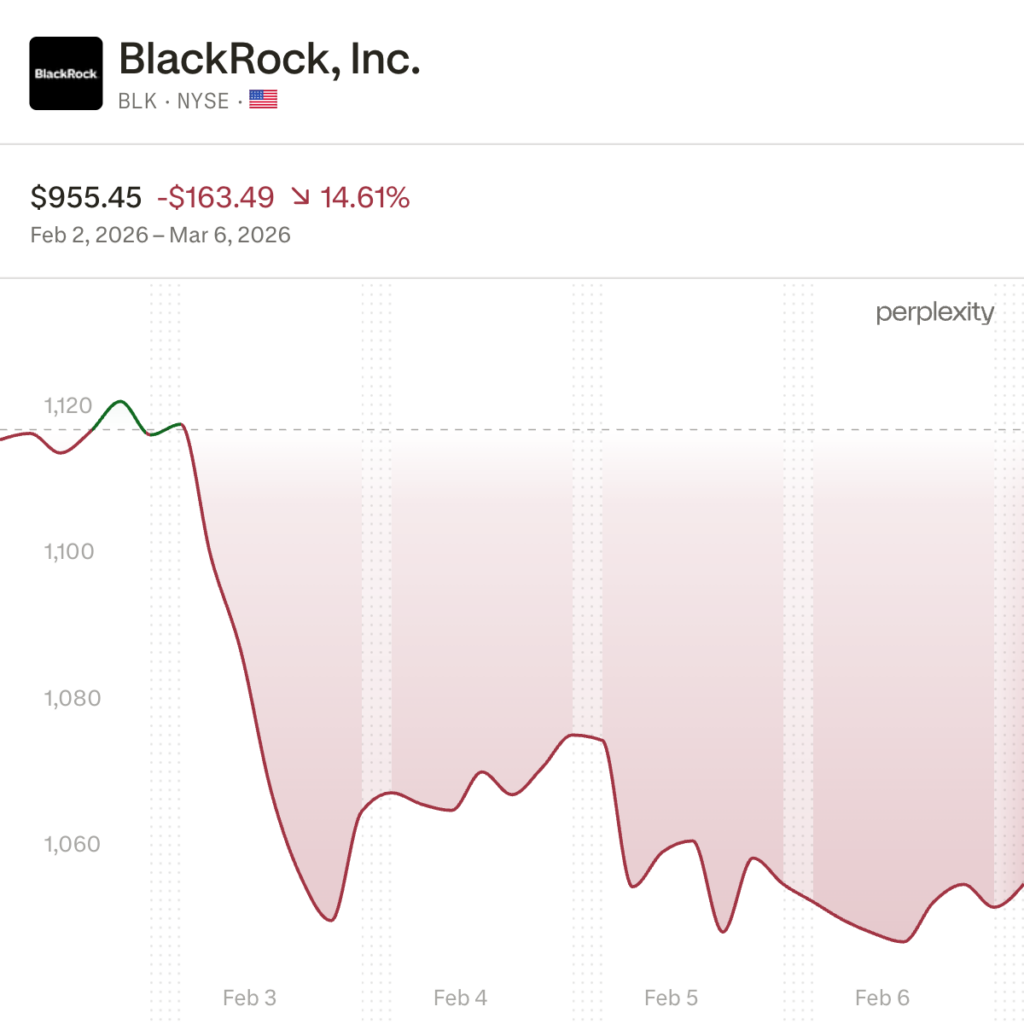

On Friday, March 6th, BlackRock gated withdrawals on its flagship $26 billion private credit fund. Redemption requests had surged beyond what the fund could absorb, and by the close of trading, the stock had fallen 6.7% in a single session.

It was not the first sign of trouble. Late last year, two U.S. firms, Tricolor and First Brands, declared bankruptcy. Then last month, UK mortgage lender MFS collapsed under allegations of fraud. It had been pledging the same collateral to multiple lenders at once, and creditors are now staring at a suspected shortfall of £930 million.

Blue Owl was actually the earlier warning. In mid-February, the firm sold $1.4 billion of loans out of its private debt funds and quietly announced it was shutting the door on quarterly redemptions for one of its retail-focused vehicles, the OBDC II fund. Withdrawal requests had surged 200% as investors grew nervous about what was sitting underneath. Management insisted this was not a halt, just a change in structure. Markets did not buy it.

Blue Owl’s shares fell for eleven straight days, the worst streak since the firm went public. Short interest climbed to an all-time high. Hedge funder Boaz Weinstein publicly offered to buy stakes in Blue Owl funds at discounts of 20% to 35%, signalling deep scepticism about the valuations the firm was reporting

“This is a canary in the coal mine,” said Dan Rasmussen of Verdad Capital. When BlackRock followed weeks later, the metaphor started to feel less like commentary and more like a diagnosis.

What Private Credit Actually is?

Private credit is simply lending that happens outside the traditional system. No public bond market, no bank syndicate. A company that needs capital goes directly to an asset manager or a private debt fund, negotiates terms, and borrows.

That simple concept now spans a wide range of strategies:

| Strategy | What It Does | Market Share |

| Direct Lending | Senior loans to mid-market companies, typically private equity-backed | ~55% |

| Asset-Based Financing (ABF) | Loans secured against assets: consumer credit, equipment, real estate | ~20% |

| Mezzanine/Junior Debt | Subordinated debt, often with equity upside | ~10% |

| Distressed/Opportunistic | Buying stressed or defaulted debt at a discount | ~8% |

| Infrastructure Debt | Long-duration loans for infrastructure projects | ~7% |

Direct lending has long been the dominant strategy, but that is shifting. Specialty finance and asset-based lending surpassed direct lending as the most popular new fund category in 2025, and capital is now spreading across more structures and more geographies than at any point in the market’s history.

At the top of the industry sit the mega-managers: Ares, Apollo, Blackstone, Blue Owl, HPS, and Golub Capital. Below them is a long tail of mid-market and regional lenders competing for deals the giants overlook. Collectively, the top ten firms control the majority of the market’s dry powder, which has now reached a record of nearly $500 billion globally.

Why the Pullback Is Happening Now

1. The Default Rate Is Worse Than It Looks

The headline default rate in private credit has stayed below 2% for years. That number flatters the market. Once you account for selective defaults, payment-in-kind toggles, and liability management exercises, the real figure is closer to 5%.

Payment-in-kind, or PIK, is when a borrower cannot afford to pay cash interest and instead rolls it into the loan balance. The debt grows quietly while the official default clock never starts. It is distress with better branding.

2. The Opacity Problem

Private loans do not trade on open markets. Valuations are set by the fund managers who own them, not by any independent price discovery. The Department of Justice recently warned publicly about creative marks and inconsistent valuation practices across private portfolios. Around the same time, the SEC launched an inquiry into a ratings agency covering private credit.

Those two things happening together are not a coincidence. When an asset class gets to price itself, stress can stay buried for a long time. Regulators are starting to take that seriously.

3. Concentration in Software

Roughly 40% of private credit loans sit in the software sector, and that sector is under real pressure. Legacy SaaS businesses are losing ground to AI-native competitors. Revenue is softening. For companies carrying significant debt loads, softer revenue means debt service starts to hurt.

For example, more than 70% of Blue Owl’s loans are to software companies, a sector already under pressure from AI disruption. Management argued the loans were senior and well-protected. The market heard something different: a heavily concentrated book, a retail investor base asking for exits, and illiquid assets that cannot be moved quickly enough to satisfy either.

A software shock would not be a contained problem for private credit. It would run straight through the middle of most portfolios.

4. The Semi-Liquid Product Problem

Private credit reached retail investors through a new class of semi-liquid vehicles: funds that promise quarterly redemptions while the underlying assets are illiquid loans that cannot be quickly sold. The pitch was yield with accessibility. The structure was always fragile.

When sentiment sours, retail investors want their money back. The loans underneath cannot move fast enough to meet them. Managers gate withdrawals. That gates confidence too. BlackRock just demonstrated exactly how that sequence plays out.

5. Macro Headwinds Are Compressing Everything

The market was already under internal stress when the external environment turned. Geopolitical conflict in the Middle East, U.S. trade uncertainty, growing skepticism around AI valuations, and a worse-than-expected jobs print on March 6th all hit in the same week. Investors moved toward safe havens quickly, and private credit was one of the first places they pulled from.

What Comes Next?

The structural case for private credit has not changed. Banks are not coming back to middle-market lending in any meaningful size. Regulatory pressure on bank balance sheets is only intensifying, particularly with Basel IV rolling out across Europe. The long-term demand for non-bank financing is real, and it is not going away because a few funds are gating redemptions.

But we believe that the easy money era is over. The managers who built their track records in a decade of low rates, loose covenants, and abundant capital are now being asked a different question: can you actually underwrite? The ones who survive this period will be the ones with genuine borrower relationships, tight documentation, and the discipline to say no to deals that do not make sense. Capital alone is no longer enough.

There is another side to this story. A new cohort of distressed and opportunistic credit funds has quietly raised over $100 billion in the past two years. They have been waiting for exactly this moment, and the same stress that is punishing weak underwriters is handing them the pipeline they built for.

Europe is quietly becoming more interesting. Spreads on comparable European private credit deals are wider than U.S. equivalents, and default rates have historically been lower. Managers with local origination in fragmented European markets may be better positioned than their U.S. peers right now.

Moody’s still projects global private credit assets under management reaching $4 trillion by 2030. That number is probably right. But the path there no longer looks like a straight line up. It runs through a shakeout that is only just beginning, and not everyone currently in this market will be around to see the other side of it.

Primary Sources

- Moody’s Private Credit 2026 Outlook: moodys.com/web/en/us/insights/credit-risk/outlooks/private-credit-2026.html

- Cleary Gottlieb, Selected Issues for Boards of Directors 2026: clearygottlieb.com/news-and-insights/publication-listing/outlook-for-private-credit-in-2026

- Chambers and Partners Private Credit 2026 Guide: practiceguides.chambers.com/practice-guides/private-credit-2026

- CNBC, Feb 20 2026 — Blue Owl withdrawal restrictions, “canary in the coal mine”: cnbc.com/2026/02/20/canary-in-the-coal-mine-blue-owl-liquidity-curbs-fuel-fears-private-credit-bubble

- CNBC, Feb 20 2026 — Blue Owl software exposure: cnbc.com/2026/02/20/blue-owl-software-lending-private-credit-concerns

- Bloomberg, Feb 22 2026 — Blue Owl 11-day losing streak: bloomberg.com/news/features/2026-02-22/blue-owl-redemptions-halt-intensifies-private-credit-fears

- Bloomberg, Mar 4 2026 — Blue Owl short interest at all-time high: bloomberg.com/news/articles/2026-03-04/blue-owl-bearish-bets-at-all-time-high-amid-private-credit-fears

- Yahoo Finance, Feb 2026 — Boaz Weinstein haircut offer: finance.yahoo.com/news/blue-owl-anxiety-rattles-1-220002807

- Reuters / U.S. News, Mar 6 2026 — BlackRock gates $26B fund: money.usnews.com/investing/news/articles/2026-03-06/blackrock-limits-withdrawals-at-private-credit-fund-as-redemptions-mount

- Within Intelligence, Jan 13 2026 — True default rate, specialty finance trends: withintelligence.com/insights/private-credit-outlook-2026

- Plante Moran, Feb 18 2026 — Tricolor, First Brands, Dimon quote, PIK risk: plantemoran.com/explore-our-thinking/insight/2026/02/private-credit-today-separating-headlines-from-reality

- PYMNTS, Mar 5 2026 — JPMorgan exposure, bank disclosures: pymnts.com/loans/2026/bank-filings-highlight-growing-exposure-volatile-private-credit-market

- Sage Advisory — DOJ warning, SEC inquiry into Egan-Jones: sageadvisory.com/article/private-credit-markets-under-pressure

- Axios, Mar 3 2026 — Blue Owl retail AUM, Blackstone redemptions: axios.com/2026/03/03/private-credit-blue-owl

- Duke University Fuqua School of Business, Sep 2025 — Institutional BDC ownership fallen to ~25

- Seeking Alpha, Feb 27 2026 — 40% software concentration: seekingalpha.com/article/4876403-its-an-early-phase-financial-crisis-the-private-credit-bust

- Carlyle 2026 Credit Outlook: carlyle.com/global-insights/research/2026-credit-outlook

- Within Intelligence — distressed funds raised $100B+: withintelligence.com/insights/private-credit-outlook-2026